Fleet Partners are companies specializing in intermediating between individuals working as Suppliers and Delivery Platforms. Working with Fleet Partners is the only way in Poland to work for Delivery Platforms without having to start your own business. A Fleet Partner employs a Supplier, earning commission on their salary. They formally handle the Supplier’s registration in the Platform application and provide (often by selling) the equipment necessary for their work. They often operate in a gray area—multiple companies operate under one name, quickly established and just as quickly abandoned, often registered as shell companies (as confirmed by a journalistic investigation in Germany, among others). Fleet Partners operate based on brutal tax optimization: Fleet Partners are shell companies, appearing and disappearing. At the same time, they play a significant role in complicating legal liability towards the employee: while the Supplier may be working for the Platform (following its instructions), they have a signed contract with the Partner and receive remuneration from them.

To secure their income, Partners try every possible means to attract Suppliers. Often, they simply manipulate information about attractive employment conditions (which is particularly susceptible to young people).

Here is our list of the 6 most common ways Fleet Partners manipulate information about working conditions:

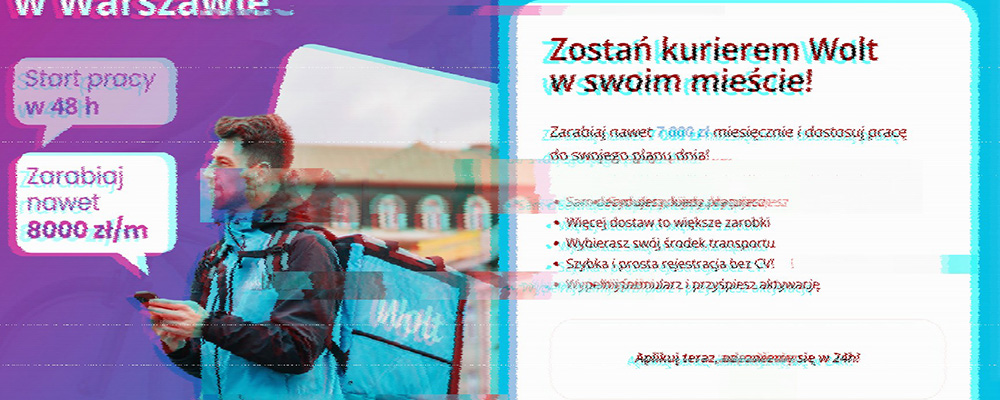

1. Advertising gross rates or “pure app income” as actual earnings

In their advertisements, Partners quote amounts such as “as much as 35 PLN per hour” or “up to 8,000 PLN per month.” This manipulation involves deducting the gross amounts from the app itself, from which the courier must subtract:

– The platform’s commission (often hidden VAT on foreign invoices)

– The fleet partner’s commission

– Taxes and social security contributions. – Fuel costs, vehicle depreciation, or bike/scooter rental.

As a result, the actual net rate can be as much as 40-50% lower than the advertised rate.

2. Hiding the “fine print” in settlement costs (so-called application fees)

Partners often tempt you with slogans like: “Only 30 PLN commission!” The provider assumes this is their only fixed cost. Only after logging into the panel or with the first payout does it become clear that the devil is in the details:

– the 30 PLN fee is charged separately for each application (e.g., if you use two applications, you pay twice).

– the fee is charged weekly, not monthly.

– additional, previously undiscussed costs arise, such as a transfer fee (2-5 PLN), a fee for issuing a personal income tax return (e.g., 50 PLN at the end of the year), or an “on-demand” funds transfer fee.

3. Constructing hybrid contracts to conceal actual tax costs

To minimize labor costs and present the supplier with a higher starting salary, partners widely use a structure: a minimal contract of mandate (e.g., for 1/100 of a full-time job or a symbolic amount) + a vehicle rental agreement. The partner does not explicitly state that the supplier must pay tax on the rental amount (taxed at a flat rate of 8.5%) or that the partner will deduct it in a complicated, difficult-to-verify manner.

Moreover, this arrangement drastically reduces social security and health insurance contributions.

4. Unsupported promises of “full assistance in legalizing residence”

This manipulation is primarily aimed at foreign suppliers. Partners lure them with slogans such as: “We will help you obtain a residence card; we provide full documentation.” In reality, to legally apply for temporary residence based on work, a stable employment contract or a reliable contract of mandate with guaranteed hours/earnings is required. The aforementioned “combined” lease agreements and low-cost contracts for services are being rejected en masse by provincial offices (Departments of Foreigners’ Affairs). Partners collect recruitment fees and commissions, while the supplier is left with useless documents.

5. Asymmetry in VAT and cost accounting (fuel, repairs)

Partners manipulate the VAT accounting method for cost invoices (e.g., fuel). Advertisements promise: “100% fuel cost deduction and VAT refund!” In practice, internal regulations say otherwise. Partners often remit only a portion of the VAT to the supplier (e.g., half), keeping the rest as an “operating expense.” Furthermore, the invoice accounting process is deliberately complicated so that the supplier refrains from submitting them, thus reducing the partner’s own income tax at the expense of the supplier’s work.

6. Opinions on forums and discussion groups

Social media (e.g., Facebook groups or Discord) are a primary source of information for new employees. Fleet Partners are well aware of this and use advanced manipulation techniques:

– Artificial promotion (Astro-turfing): Marketing staff or bots create fictitious accounts en masse to recommend a specific Partner in discussions under posts.

It often looks like a natural conversation (“I go there too, my pay is always on time, I recommend the company”), when in reality, it’s a completely staged post.

– Deleting and censoring criticism: Many popular discussion groups and local forums for suppliers are moderated or even sponsored by Fleet Partners. Posts describing late payments, hidden contractual penalties, or lack of support contact are immediately deleted, and the authors are blocked. This creates a false image of a company that supposedly has no dissatisfied employees.

Many other methods could be added to this list. For example, organizing “Fleet Partner Open Houses,” during which you can “casually” inquire about working conditions, eat a free candy bar, drink an energy drink, or even receive a “free backpack.”

And also:

THERE ARE 5 MONTHS AND 22 DAYS LEFT TO IMPLEMENT THE PLATFORM WORK DIRECTIVE.